Yields Move Higher, Along with Investor Anxiety

- While this week has been light on new economic data, and frankly not much new on the Middle East front either, yields are becoming the main story. Longer duration yields are moving to near 20yr highs and it’s a global pattern, not just a domestic issue. Today’s highlights will again be limited, with FOMC minutes the only item of consequence, and given the inflation news from last week and the subsequent move in rates this week, the discussions will have a stale taste to them. Currently, the 10yr is yielding 4.64%, down 3bps in early trading. The 2yr is yielding 4.09%, also down 3bps. Meanwhile, the 30yr is at 5.17%, the highest in a year.

- Bond yields have moved centerstage with the relentless increase that has taken place since the start of military operations in Iran, and it’s been a global phenomenon. The graph below tracks 10yr yields across four of the largest developed sovereign debt markets, and all are at or very near 20yr highs in yields. Only the UK and Germany remain under yields from 2007 but they’re gaining fast. History tells us that when yields move to this degree, and especially with the acceleration in 2026, something usually breaks somewhere. The question is where and when?

- Less developed markets that trade domestic debt in US dollars are often the first to cry “Uncle” as currency risk adds to the misery of higher yields, so that’s where the immediate focus lies. But across the globe, the specter of higher yields will have a negative impact on growth and adds expenses to budgets already struggling with higher commodity prices. Domestically, we’ve avoided a major equity correction to this point, but if it happens it no doubt will dampen consumption among the more well-heeled consumer that has kept spending elevated during this period.

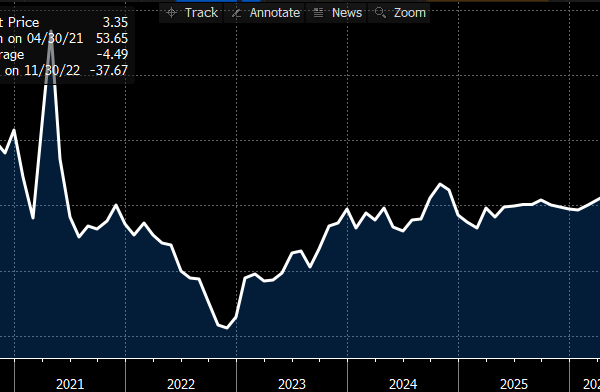

- Meanwhile, the paradox of our economy continues as the weekly ADP Pulse Report for the week ending May 2, 2026, found 42,250 new private sector jobs. That represents a high for the series and the second straight week of increasing job growth. The report uses a four-week average, so the May 2nd reading encompasses most of April which confirms much of the headline job growth reported in the April BLS Nonfarm Payrolls Report. The caveat is that while it’s a weekly report it’s somewhat backward looking given we’re two weeks beyond May 2nd and the four-week average methodology includes older data. Still, three of the last six weekly averages have topped 40 thousand jobs which points to increasing momentum, albeit not the latest read of what is happening in May (see graph below).

- Yet another paradox, if you thought higher yields would put a dent in housing/mortgage activity, well, that’s a reasonable assumption but it wasn’t what happened in April. Pending home sales rose 1.4%, a five-month high, beating the 1.0% forecast. Year-over-year sales increased 3.3% (see graph below). The results suggest housing is/was finding some footing entering the busiest selling time of year, and results were aided in April as mortgage rates dipped in the second half of the month. In May, however, rates reversed and are heading higher, along with Treasury yields. Pending home sales provides the timeliest housing activity indicator as they’re based on contract signings and not closings which take a month or two longer to complete, so we remain unconvinced a durable rebound in housing is upon us, and thus we wait for May data.

- Away from higher yields, investors might be distracted by the April 29th FOMC Minutes due at 2pm ET. With the inflation news from last week, and the upward march in rates, any discussion of possible rate cuts will be put aside, and instead, the minutes will be scoured for any discussions of inflation risk and thoughts of possible rate hikes. Also, with the three dissents wanting a move to a neutral bias from an easing one we’ll be attuned to the discussions around that matter. New Fed Chair Kevin Warsh will preside over the June meeting, and his rate-cutting bias will most likely be put aside. As we mentioned on Monday, look for his initial focus to be in a messaging shift with a reduction in forward guidance, including the elimination of the controversial Dot Plots.

Sovereign 10yr Debt Yields Move to Near 20yr Highs

Source: Bloomberg

Weekly ADP Pulse Report (as of May 2nd) – Private Sector Hiring Continues Moving Higher Source: ADP

Source: ADP

Pending Home Sales (YoY) – Enjoyed a Nice Bounce in April but Higher Rates are Expected to Dent Future Activity Source: NAR

Source: NAR

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.